2026 Housing Market Forecast: Buying vs. Renting Decisions

The housing market is a perennial topic of discussion, a cornerstone of personal finance, and a significant driver of the global economy. As we inch closer to the middle of the decade, attention is increasingly turning towards the 2026 housing forecast. For many, this isn’t just an academic exercise; it’s a critical financial planning endeavor, especially when weighing the monumental decision of buying a home versus continuing to rent. The landscape of real estate is constantly shifting, influenced by a myriad of economic, social, and technological factors. Understanding these dynamics is paramount for anyone looking to make informed choices in the coming years.

The past few years have been a rollercoaster for real estate, marked by unprecedented price surges, fierce competition, and then a period of recalibration driven by rising interest rates. This volatility has left many prospective homeowners and even seasoned investors feeling uncertain about what lies ahead. Will the market stabilize? Will prices continue to climb, or are we on the brink of a significant correction? These are the questions that define the current discourse around the 2026 housing forecast. This comprehensive analysis aims to dissect the various components that will likely shape the housing market in 2026, providing a clearer picture for your financial future.

Our exploration will delve into the critical economic indicators that historically influence housing trends, such as interest rates, inflation, and unemployment. We’ll also examine the supply and demand dynamics, which remain fundamental to price movements. Furthermore, we will consider the impact of demographic shifts, evolving work-from-home trends, and policy decisions that could either fuel or cool the market. By piecing together these complex elements, we hope to offer a nuanced and actionable perspective on the 2026 housing forecast, empowering you to navigate the real estate market with greater confidence.

Understanding the Economic Undercurrents: What Drives the 2026 Housing Forecast?

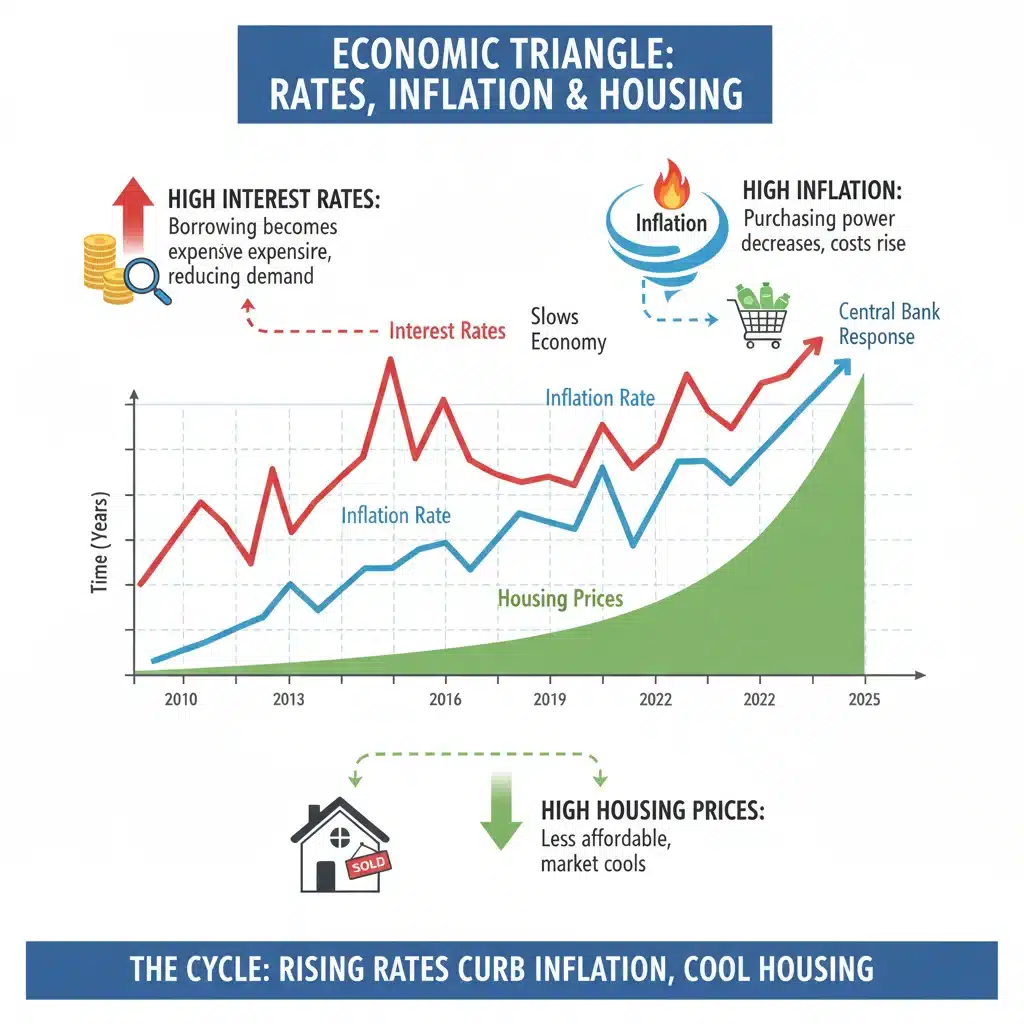

To truly grasp the potential direction of the 2026 housing forecast, we must first understand the fundamental economic forces at play. The housing market does not exist in a vacuum; it is intricately linked to broader economic health and monetary policy. Three of the most influential factors are interest rates, inflation, and the overall state of the job market.

Interest Rates: The Cost of Borrowing

Interest rates are arguably the most direct and impactful factor on housing affordability and demand. When interest rates are low, the cost of borrowing money for a mortgage is cheaper, making homeownership more accessible and stimulating demand. Conversely, when rates rise, mortgage payments become more expensive, effectively pricing some buyers out of the market and dampening demand. The Federal Reserve’s decisions on the federal funds rate have a ripple effect across the entire financial system, including mortgage rates.

Looking towards the 2026 housing forecast, many economists predict a period of relative stability, or even a slight decline, in interest rates compared to the peaks seen in recent years. However, this largely depends on the trajectory of inflation and the Fed’s ongoing battle to bring it to its target levels. If inflation proves more stubborn than anticipated, rates could remain elevated, continuing to exert downward pressure on housing demand and potentially leading to more moderate price growth or even modest declines in some areas. Conversely, if inflation is successfully tamed, the Fed might have more leeway to cut rates, which could reinvigorate buyer interest and support housing values. The precise path of interest rates will be a defining characteristic of the 2026 housing forecast.

Inflation: Erosion of Purchasing Power

Inflation, the rate at which the general level of prices for goods and services is rising, has a complex relationship with the housing market. On one hand, high inflation can erode purchasing power, making it harder for individuals to save for a down payment and afford higher mortgage payments. On the other hand, real estate is often considered a hedge against inflation, as property values and rents tend to increase alongside general price levels over the long term. This dual impact makes inflation a critical component in understanding the 2026 housing forecast.

If inflation remains elevated, it could prompt the Federal Reserve to keep interest rates higher for longer, as discussed previously, thereby cooling the housing market. However, if inflation moderates, it could pave the way for lower interest rates, making housing more affordable. The interplay between inflation and interest rates is a delicate balancing act that will significantly influence both the demand side and the investment appeal of real estate in 2026. A stable, controlled inflation environment would be ideal for a healthy housing market, allowing for sustainable growth without the pressures of rapidly rising costs.

Job Market and Wages: The Foundation of Affordability

A robust job market with strong wage growth is the bedrock of a healthy housing market. When people are employed and earning good incomes, they have the financial capacity and confidence to purchase homes. Conversely, high unemployment or stagnant wages can cripple housing demand. The 2026 housing forecast will heavily depend on the strength and stability of the labor market.

Current projections suggest a relatively stable job market leading into 2026, though some sectors may experience shifts due to technological advancements and economic restructuring. Continued wage growth, especially if it outpaces inflation, would be a positive sign for housing affordability. It would enable more individuals to save for down payments and manage mortgage costs. Any significant downturn in employment or a deceleration in wage gains could pose a challenge to the housing market, potentially leading to increased inventory and more competitive pricing for sellers. Therefore, monitoring labor market indicators will be crucial for anyone assessing the 2026 housing forecast.

Supply and Demand Dynamics: The Core of the 2026 Housing Forecast

Beyond macroeconomic factors, the fundamental principles of supply and demand dictate property values. The balance between the number of available homes for sale and the number of eager buyers is a primary driver of price appreciation or depreciation. Understanding these dynamics is essential for any accurate 2026 housing forecast.

Housing Inventory: A Persistent Challenge

For years, the housing market has grappled with a significant shortage of available homes. This under-supply, a legacy of underbuilding after the 2008 financial crisis, has been a key factor in driving up prices. While new construction has picked up in some areas, it often struggles to keep pace with demand, especially in rapidly growing urban and suburban centers. The 2026 housing forecast will largely hinge on whether new construction can meaningfully bridge this gap.

Factors affecting inventory include the cost of materials and labor, zoning regulations, and the willingness of existing homeowners to sell. Many homeowners with historically low mortgage rates are hesitant to sell and buy a new home at a higher rate, further constraining supply. If this trend continues into 2026, inventory levels may remain tight, supporting prices. However, a significant increase in new home builds or a loosening of existing homeowners’ grip on their low-rate mortgages could bring more supply to the market, potentially easing price pressures.

Buyer Demand: Demographic Shifts and Affordability

On the demand side, several factors will shape the 2026 housing forecast. Demographics play a huge role, particularly the large millennial generation entering their prime home-buying years. This cohort, despite facing affordability challenges, still represents a massive wave of potential buyers. Their preferences for location, home type, and amenities will influence market trends.

Affordability, as mentioned, is a critical constraint. High prices combined with elevated interest rates have pushed homeownership out of reach for many. If interest rates moderate and wage growth continues, affordability could improve, reigniting demand. Conversely, if these conditions worsen, demand could soften further. The balance between this underlying demographic demand and the actual affordability constraints will be a key determinant of the 2026 housing forecast.

Regional Variations: Not a Monolithic Market

It’s crucial to remember that the housing market is not a single entity; it’s a collection of local markets, each with its own unique characteristics. A national 2026 housing forecast provides a general overview, but the reality on the ground can vary dramatically from one region to another, or even from one neighborhood to the next.

Booming Regions vs. Stagnant Areas

Some areas, particularly those with strong job growth, diverse economies, and attractive lifestyles, are likely to continue experiencing robust demand and potentially higher price appreciation. Tech hubs, emerging industrial centers, and areas with favorable tax policies often fall into this category. Conversely, regions experiencing population decline, economic stagnation, or oversupply could see more muted growth or even price declines. When considering the 2026 housing forecast, it’s vital to research specific local market conditions.

Factors such as local government policies, infrastructure development, and climate migration (e.g., people moving due to extreme weather events) will also play an increasingly important role in shaping regional housing markets. These localized dynamics can significantly alter the national outlook for individual buyers and investors. Therefore, a granular approach is necessary when applying any broad 2026 housing forecast to personal decisions.

Buying vs. Renting in 2026: A Financial Perspective

With the complexities of the 2026 housing forecast laid out, the central question for many remains: Is it better to buy or rent? This decision is deeply personal and depends on individual financial circumstances, lifestyle preferences, and long-term goals. However, the economic climate of 2026 will undoubtedly influence the financial calculus.

The Case for Buying in 2026

For those with stable finances, a solid down payment, and a long-term perspective, buying a home in 2026 could still be a sound investment. If interest rates stabilize or slightly decline, and if inflation moderates, the long-term benefits of homeownership – wealth accumulation through equity, potential tax benefits, and stability of housing costs (especially with a fixed-rate mortgage) – remain compelling. A well-researched purchase in a fundamentally strong market could provide significant returns over time.

The 2026 housing forecast suggests that while rapid appreciation seen in 2020-2022 is unlikely to return, steady, sustainable growth is a reasonable expectation in many areas. For those who view a home as a long-term asset and a place to build roots, buying can offer a sense of permanence and control that renting cannot. However, buyers must be prepared for the ongoing costs of maintenance, property taxes, and insurance, which can add substantially to monthly expenses beyond the mortgage payment.

The Case for Renting in 2026

Renting offers flexibility, which is particularly appealing for those who are uncertain about their long-term location, career path, or family plans. It also frees individuals from the responsibilities and costs of home maintenance, property taxes, and unexpected repairs. In a market where home prices are high and interest rates are elevated, renting can often be the more affordable monthly option, allowing individuals to save and invest their money elsewhere.

If the 2026 housing forecast points to continued high prices and rates, or even a potential market correction in certain areas, renting could be the financially prudent choice. It allows individuals to save for a larger down payment, wait for more favorable market conditions, or invest in other assets that might offer better returns in the short to medium term. The key is to analyze the ‘rent vs. buy’ ratio in your desired location and consider your personal financial goals. If renting allows you to save significantly more or provides crucial flexibility, it may be the superior option for 2026.

Key Factors to Consider for Your 2026 Housing Decision

Beyond the broad strokes of the 2026 housing forecast, several specific personal and market factors should guide your decision-making process:

Personal Financial Health

- Down Payment Savings: Do you have sufficient funds for a down payment (typically 5-20% of the home price)? The larger the down payment, the less you need to borrow and the lower your monthly payments.

- Credit Score: A strong credit score is crucial for securing the best mortgage rates. Work on improving your credit if it’s not in optimal shape.

- Debt-to-Income Ratio: Lenders assess your ability to manage monthly payments. Keep your existing debt low relative to your income.

- Emergency Fund: Homeownership comes with unexpected costs. A robust emergency fund is non-negotiable.

Market Indicators to Watch

- Local Inventory Levels: Is your desired market experiencing a shortage or surplus of homes? High inventory favors buyers, low inventory favors sellers.

- Median Home Prices: Track the trend of home prices in your target areas. Are they appreciating, depreciating, or stabilizing?

- Rental Costs vs. Mortgage Costs: Compare what you’d pay in rent versus a potential mortgage payment (including taxes, insurance, and HOA fees).

- Interest Rate Trends: Keep a close eye on forecasts for mortgage rates. Even a small change can significantly impact affordability.

Long-Term Goals and Lifestyle

- Duration of Stay: If you plan to move within 2-5 years, buying might not be financially advantageous due to transaction costs (closing costs, realtor fees). Renting offers more flexibility.

- Desired Lifestyle: Do you value the freedom from maintenance that renting provides, or do you prefer the autonomy and personalization of homeownership?

- Investment Diversification: Consider how homeownership fits into your overall investment portfolio. Could your capital be better deployed elsewhere if you rent?

Expert Predictions and Consensus for the 2026 Housing Forecast

While no one has a crystal ball, many leading real estate economists and financial institutions offer their projections for the coming years. For the 2026 housing forecast, a general consensus seems to point towards a more balanced market compared to the extremes of recent years.

Many experts predict that home price growth will likely moderate, potentially aligning more closely with historical averages of 3-5% annually, rather than the double-digit surges seen previously. Some areas that experienced the most dramatic price increases might even see slight corrections, while others with strong fundamentals could continue to see steady appreciation. The expectation is that interest rates, while potentially lower than their recent peaks, will not return to the ultra-low levels of the pandemic era, meaning affordability will remain a key challenge.

Inventory levels are expected to remain somewhat constrained, though new construction might gradually ease some of the pressure. The rental market is also projected to stabilize, with rent growth moderating after significant increases. Ultimately, the 2026 housing forecast is less about a dramatic boom or bust and more about a return to more sustainable, albeit still competitive, conditions.

Navigating the 2026 Housing Market: Strategies for Success

Regardless of whether you decide to buy or rent, being prepared is key to navigating the 2026 housing forecast successfully. Here are some actionable strategies:

For Prospective Buyers:

- Get Pre-Approved for a Mortgage: Understand exactly what you can afford and demonstrate your seriousness to sellers.

- Save Aggressively: A larger down payment can reduce your monthly costs and make your offer more attractive.

- Be Flexible: Consider a wider range of neighborhoods or property types if your initial preferences are out of budget.

- Work with a Knowledgeable Agent: A local real estate expert can provide invaluable insights into specific market conditions and opportunities.

- Factor in All Costs: Remember closing costs, property taxes, insurance, and potential maintenance when budgeting.

For Renters:

- Budget Wisely: Allocate a realistic portion of your income to rent and other living expenses.

- Build Your Savings: Use the flexibility of renting to build a substantial emergency fund and save for future goals, whether that’s a down payment or other investments.

- Monitor the Market: Keep an eye on housing prices and interest rates. If conditions become more favorable for buying, you’ll be ready to pivot.

- Negotiate Rent: In some markets, especially if supply increases, you might have room to negotiate rent prices or lease terms.

Conclusion: A Balanced Outlook for the 2026 Housing Forecast

The 2026 housing forecast paints a picture of a market that is evolving from the frenetic pace of recent years towards a more measured and potentially stable environment. While challenges like affordability and inventory shortages will persist, a moderation in interest rates and a stable job market could provide a more balanced playing field for both buyers and sellers.

The decision to buy or rent in 2026 will continue to be a deeply personal one, influenced by individual financial health, career trajectory, and lifestyle preferences. There is no one-size-fits-all answer. By understanding the key economic drivers – interest rates, inflation, and employment – alongside the dynamics of supply and demand, and by being aware of regional variations, you can make an informed choice that aligns with your long-term financial goals.

Staying informed, consulting with financial advisors and real estate professionals, and carefully evaluating your personal circumstances against the backdrop of the 2026 housing forecast will be your best strategy for success. The real estate journey is a marathon, not a sprint, and thoughtful planning will yield the most rewarding outcomes.