Optimizing Your Retirement Portfolio for 2026: Strategies to Achieve a 7% Annual Return

As we approach 2026, many individuals are re-evaluating their financial goals and seeking robust strategies to ensure a secure and comfortable retirement. The ambitious yet achievable target of a 7% annual return on your Retirement Portfolio 2026 requires a strategic, disciplined, and informed approach. This comprehensive guide will delve into the critical aspects of building and managing a retirement portfolio designed to meet or even exceed this growth target, navigating the complexities of the market, and leveraging diversification for sustainable success.

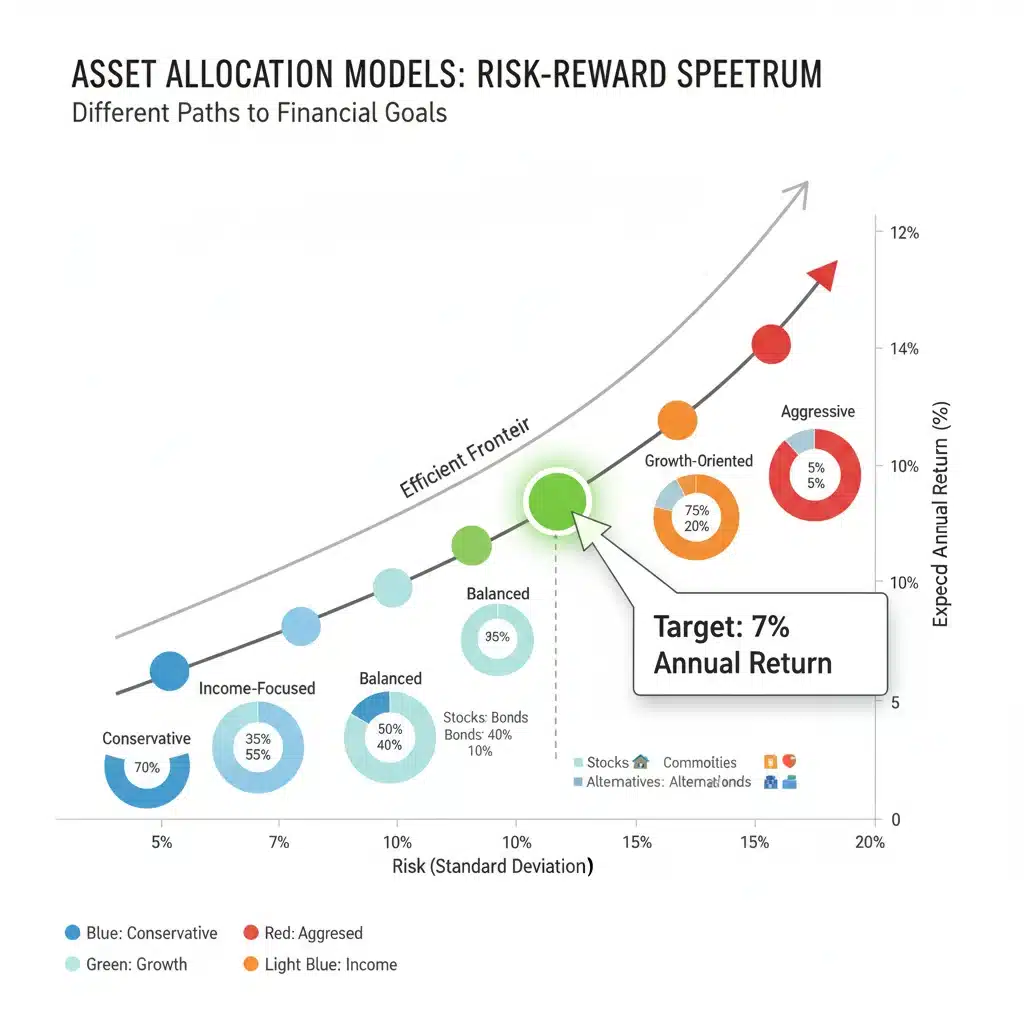

Understanding the 7% Annual Return Goal for Your Retirement Portfolio 2026

A 7% annual return is often considered a healthy benchmark for long-term investment growth, especially within a retirement context. It’s a rate that, over time, can significantly outpace inflation and contribute substantially to wealth accumulation. However, achieving this consistently by 2026 and beyond isn’t a matter of luck; it demands careful planning, a clear understanding of market dynamics, and a proactive investment strategy. The landscape for your Retirement Portfolio 2026 will be shaped by various global economic factors, technological advancements, and evolving market conditions. Therefore, flexibility and adaptability are key.

Why 7%? The Power of Compounding

The magic behind the 7% annual return lies in the power of compounding. When your investments generate returns, and those returns themselves start earning returns, your wealth grows exponentially. Over decades, even seemingly small differences in annual returns can translate into substantially different retirement nest eggs. For instance, a starting capital of $100,000 earning 7% annually would grow to significantly more than one earning 4% over a 20-30 year period, highlighting the importance of targeting a robust growth rate for your Retirement Portfolio 2026.

Pillars of a High-Performing Retirement Portfolio 2026

Building a retirement portfolio capable of generating a 7% annual return requires a multi-faceted approach. Here are the core pillars to consider:

1. Strategic Asset Allocation: The Foundation of Your Retirement Portfolio 2026

Asset allocation is arguably the most crucial decision you’ll make for your Retirement Portfolio 2026. It involves dividing your investment capital among different asset classes, such as stocks, bonds, real estate, and cash equivalents. The ideal allocation depends on your age, risk tolerance, time horizon, and financial goals. For a 7% annual return, a growth-oriented allocation is typically necessary, often leaning more towards equities while maintaining a sensible level of diversification to mitigate risk.

Equity Investments: Driving Growth

- Growth Stocks: Companies with high growth potential, often in technology, healthcare, or emerging markets, can provide significant capital appreciation. However, they come with higher volatility.

- Dividend Stocks: Mature companies that pay regular dividends can offer a stable income stream and some capital appreciation, acting as a buffer during market downturns.

- Index Funds and ETFs: These passively managed funds offer broad market exposure and diversification at a low cost, often outperforming actively managed funds over the long term. They are excellent choices for the core of your Retirement Portfolio 2026.

Fixed Income: Stability and Income

While equities drive growth, fixed-income investments like bonds provide stability and income. They can help cushion your portfolio during market downturns. For a 7% return target, you might consider a smaller allocation to traditional government bonds and explore higher-yielding corporate bonds or bond ETFs with careful consideration of credit risk.

Alternative Investments: Enhancing Diversification and Return Potential

To further optimize your Retirement Portfolio 2026 for higher returns, consider a modest allocation to alternative investments. These can include:

- Real Estate: Through REITs (Real Estate Investment Trusts) or direct investments, real estate can offer inflation protection and rental income.

- Commodities: Gold, silver, and other commodities can act as hedges against inflation and market volatility.

- Private Equity/Debt: While less liquid, these can offer higher returns for sophisticated investors.

The key is to balance the growth potential of these assets with their inherent risks and liquidity considerations within your Retirement Portfolio 2026.

2. Risk Management: Protecting Your Retirement Portfolio 2026

Achieving a 7% annual return doesn’t mean taking reckless risks. Effective risk management is paramount. This involves understanding the various types of risks (market risk, inflation risk, interest rate risk, credit risk) and implementing strategies to mitigate them.

Diversification Beyond Asset Classes

True diversification extends beyond just different asset classes. It includes:

- Geographic Diversification: Investing in international markets can reduce reliance on a single economy and tap into growth opportunities worldwide.

- Sector Diversification: Spreading investments across various industries minimizes the impact of a downturn in any single sector.

- Time Diversification (Dollar-Cost Averaging): Investing a fixed amount regularly, regardless of market fluctuations, can reduce the average cost per share over time and smooth out volatility. This is a powerful strategy for building your Retirement Portfolio 2026.

Regular Rebalancing

Over time, market fluctuations can cause your asset allocation to drift from your target. Regular rebalancing (e.g., annually or semi-annually) involves selling off assets that have grown significantly and reinvesting in those that have underperformed, bringing your portfolio back to its desired allocation. This helps maintain your risk profile and can even enhance returns.

3. Cost Management: Maximizing Net Returns for Your Retirement Portfolio 2026

Every dollar spent on fees, commissions, and taxes is a dollar not working for you. Minimizing these costs can significantly impact your net returns, bringing you closer to your 7% annual goal for your Retirement Portfolio 2026.

- Low-Cost Index Funds and ETFs: These typically have much lower expense ratios compared to actively managed mutual funds.

- Tax-Efficient Investing: Utilizing tax-advantaged accounts like 401(k)s, IRAs, and Roth IRAs can shield your investments from taxes, allowing them to grow faster. Understanding capital gains taxes and tax-loss harvesting can also be beneficial.

- Avoiding Excessive Trading: Frequent buying and selling can incur transaction costs and potentially higher taxes. A long-term, buy-and-hold strategy is often more cost-effective.

Leveraging Market Trends and Economic Outlook for Your Retirement Portfolio 2026

While a long-term perspective is crucial, being aware of prevailing market trends and the economic outlook for 2026 can help you make informed adjustments to your Retirement Portfolio 2026.

Inflation and Interest Rates

The trajectory of inflation and interest rates will significantly impact bond yields and the valuation of growth stocks. High inflation can erode purchasing power, making investments that offer inflation protection (like real estate or certain commodities) more attractive. Rising interest rates can make bonds more appealing but can also increase borrowing costs for companies, potentially impacting equity performance. Monitoring these indicators is vital for your Retirement Portfolio 2026.

Technological Advancements and Sector Growth

Sectors driven by innovation, such as artificial intelligence, renewable energy, biotechnology, and cybersecurity, are likely to continue experiencing significant growth. Allocating a portion of your Retirement Portfolio 2026 to these sectors through specific ETFs or individual stocks can provide substantial upside potential, albeit with higher risk.

Global Economic Growth

Understanding the economic health of major global economies (US, Europe, China, emerging markets) can inform your geographic diversification strategy. Strong growth in certain regions might present compelling investment opportunities that can contribute to your 7% annual return goal.

Advanced Strategies for Your Retirement Portfolio 2026

For those comfortable with a slightly higher level of complexity, certain advanced strategies can further enhance your chances of hitting the 7% annual return target for your Retirement Portfolio 2026.

Factor Investing

Factor investing involves targeting specific characteristics or ‘factors’ that have historically led to higher returns or lower risk. Examples include:

- Value: Investing in undervalued companies.

- Momentum: Investing in stocks that have been performing well.

- Size: Investing in small-cap companies, which historically have higher growth potential.

- Quality: Investing in companies with strong balance sheets and consistent earnings.

Factor-based ETFs are readily available and can be integrated into your Retirement Portfolio 2026.

Income-Generating Strategies

Beyond traditional dividends and bond interest, consider strategies like:

- Covered Call Writing: For experienced investors, selling covered calls on existing stock holdings can generate additional income.

- High-Yield Bonds: While riskier, these can offer higher income streams. Careful research into the creditworthiness of issuers is essential.

Considering Professional Guidance for Your Retirement Portfolio 2026

Navigating the complexities of investment markets and optimizing your Retirement Portfolio 2026 can be challenging. A qualified financial advisor can provide personalized advice, help you define your risk tolerance, set realistic goals, and construct a portfolio tailored to your specific needs. They can also assist with tax planning and estate planning, which are integral parts of a comprehensive retirement strategy.

Monitoring and Adjusting Your Retirement Portfolio 2026

Building a robust retirement portfolio is not a one-time event. It requires continuous monitoring and periodic adjustments. The economic landscape, your personal circumstances, and market valuations are constantly changing. Therefore, regularly reviewing your Retirement Portfolio 2026 is crucial.

Regular Portfolio Reviews

Schedule at least annual reviews of your portfolio. During these reviews, assess:

- Performance: Is your portfolio on track to meet the 7% annual return target?

- Asset Allocation: Has your allocation drifted significantly from your target?

- Risk Tolerance: Has your comfort level with risk changed?

- Life Events: Have there been any significant life changes (marriage, children, career changes) that warrant adjustments to your financial plan?

- Market Conditions: Are there any new market opportunities or risks that need to be addressed?

Adapting to Market Cycles

Markets operate in cycles, and understanding these cycles can help you make informed decisions. While timing the market is notoriously difficult, recognizing broader trends can guide your rebalancing decisions. For instance, during periods of overvaluation in certain sectors, it might be prudent to trim positions and reallocate to more reasonably valued assets within your Retirement Portfolio 2026.

Staying Informed

Continuous learning about personal finance, investment strategies, and economic news is invaluable. Reputable financial news sources, books, and educational seminars can equip you with the knowledge needed to make sound decisions for your Retirement Portfolio 2026.

Common Pitfalls to Avoid When Aiming for 7% Annual Returns

While aiming for a 7% annual return, it’s equally important to be aware of common mistakes that can derail your progress:

- Emotional Investing: Making investment decisions based on fear or greed, often leading to buying high and selling low.

- Lack of Diversification: Concentrating too much capital in a single stock, sector, or asset class.

- Ignoring Fees: Underestimating the long-term impact of high management fees and trading costs.

- Chasing Hot Trends: Investing in popular but potentially overvalued assets without proper due diligence.

- Insufficient Savings: Even with a strong return, insufficient capital can hinder your retirement goals. Consistent contributions to your Retirement Portfolio 2026 are vital.

- Not Adjusting for Inflation: Failing to account for the eroding effect of inflation on your future purchasing power.

Case Study: A Hypothetical Retirement Portfolio 2026 Strategy

Let’s consider a hypothetical individual, Sarah, aged 45, aiming for a 7% annual return for her Retirement Portfolio 2026 over the next 20 years. Her current portfolio is $500,000, and she contributes $1,000 monthly.

Sarah’s Proposed Asset Allocation:

- 65% Equities:

- 30% U.S. Large-Cap Index Fund (e.g., S&P 500 ETF)

- 15% International Developed Markets Index Fund

- 10% Emerging Markets Index Fund

- 10% Growth-Oriented Sector ETF (e.g., Technology or Healthcare)

- 25% Fixed Income:

- 15% Investment-Grade Corporate Bond ETF

- 10% U.S. Treasury Bond ETF (for stability)

- 10% Alternative Investments:

- 5% REIT ETF

- 5% Gold ETF

Strategy Implementation:

- Dollar-Cost Averaging: Sarah consistently invests $1,000 each month into her chosen funds.

- Annual Rebalancing: At the end of each year, Sarah reviews her portfolio and rebalances to maintain her target asset allocation.

- Tax Efficiency: She utilizes her 401(k) and Roth IRA accounts for maximum tax benefits.

- Continuous Learning: Sarah stays informed about market conditions and global economic trends.

This diversified approach, combined with regular contributions and disciplined management, significantly increases Sarah’s probability of achieving her 7% annual return goal for her Retirement Portfolio 2026 and securing her financial future.

Conclusion: Your Path to a 7% Annual Return for Retirement Portfolio 2026

Achieving a 7% annual return on your Retirement Portfolio 2026 is an ambitious yet entirely attainable objective with the right strategies in place. It demands a commitment to strategic asset allocation, diligent risk management, cost-effective investing, and continuous learning. By understanding the power of compounding, diversifying your investments across various asset classes and geographies, minimizing fees, and staying informed about market dynamics, you can significantly enhance your chances of reaching your retirement goals.

Remember that investing involves risk, and past performance is not indicative of future results. However, by adopting a disciplined, long-term approach and making informed decisions, you can build a resilient and high-performing Retirement Portfolio 2026 that provides the financial security you deserve in your golden years. Start planning today, review regularly, and stay committed to your financial future.

in 2025: Maximize Returns with New Contribution Limits")

by 15%")