Mastering Interest Rate Hikes: Loan Strategies for 2026 Savings

The Latest Interest Rate Hikes: How to Adjust Your Loan Strategies for 2026 to Save Thousands Annually

As we approach 2026, the financial landscape continues its dynamic shift, with interest rate hikes becoming a prominent feature. For many, this brings a mix of uncertainty and concern, especially regarding existing loans and future borrowing. Understanding how to navigate these changes is not just about staying afloat; it’s about strategically adjusting your loan strategies to potentially save thousands annually. This comprehensive guide will delve into the anticipated interest rate environment for 2026, explore its impact on various loan types, and provide actionable strategies to protect and optimize your financial health.

Understanding the 2026 Interest Rate Outlook

Before we dive into specific loan strategies, it’s crucial to grasp the prevailing economic sentiment and expert predictions for interest rates in 2026. Central banks worldwide have been employing interest rate adjustments as a primary tool to manage inflation and stabilize economies. While the exact trajectory can be unpredictable, the general consensus points towards a continued period of elevated rates, albeit with potential plateaus or minor adjustments based on economic indicators.

Factors Influencing Interest Rate Hikes

Several key factors contribute to the interest rate environment. Understanding these can help you anticipate future movements and refine your loan strategies:

- Inflation: Persistently high inflation is a major driver for central banks to raise interest rates, making borrowing more expensive to cool down economic activity.

- Economic Growth: Strong economic growth can also lead to higher rates as demand for capital increases. Conversely, a slowdown might prompt central banks to ease rates.

- Geopolitical Events: Global events, such as conflicts or trade disputes, can introduce volatility and influence central bank decisions.

- Labor Market Strength: A robust job market, often associated with wage growth, can contribute to inflationary pressures, leading to higher rates.

- Government Fiscal Policy: Government spending and borrowing can also impact market liquidity and, consequently, interest rates.

For 2026, many economists anticipate that while the aggressive hikes seen in previous years might temper, rates will likely remain above pre-pandemic levels. This ‘new normal’ necessitates a proactive approach to managing your debt and adopting effective loan strategies.

Impact of Rising Interest Rates on Various Loan Types

The effect of rising interest rates isn’t uniform across all loan types. Understanding these nuances is essential for developing targeted loan strategies.

Mortgages: Variable vs. Fixed Rates

Your mortgage is likely your largest debt, and rising interest rates can have a significant impact. If you have a variable-rate mortgage, your monthly payments will directly increase with rate hikes. For fixed-rate mortgages, your payments remain stable until renewal, but new borrowers or those renewing in 2026 will face higher rates.

- Variable-Rate Mortgages: Immediate impact on monthly payments, increasing your cost of borrowing.

- Fixed-Rate Mortgages: Payments are locked in, but renewal in a high-rate environment means significantly higher future payments.

Personal Loans and Lines of Credit

Many personal loans have fixed rates, meaning your payments won’t change. However, if you have a variable-rate personal loan or a line of credit, your interest payments will increase. This can quickly erode your budget and make it harder to pay down the principal.

Credit Card Debt

Credit card interest rates are almost always variable and are among the first to react to central bank rate hikes. Carrying a balance on credit cards becomes significantly more expensive, making it a priority to pay off high-interest credit card debt as part of your loan strategies.

Auto Loans

Most auto loans are fixed-rate. However, if you’re planning to purchase a new vehicle in 2026, you’ll likely face higher borrowing costs, increasing your overall car payment. Refinancing an existing auto loan might also be less attractive in a high-rate environment, but it depends on your current rate.

Student Loans

Federal student loans often have fixed rates, but private student loans can be variable. For those with variable-rate private student loans, payments will increase. New student loans taken out in 2026 will also reflect the higher interest rate environment.

Proactive Loan Strategies to Save Thousands Annually

Now that we understand the landscape, let’s explore concrete loan strategies you can implement to mitigate the impact of rising interest rates and potentially save a substantial amount of money.

1. Prioritize High-Interest Debt Repayment

This is perhaps the most critical strategy. Debts with the highest interest rates, typically credit cards and some personal loans, should be your primary focus. The ‘debt avalanche’ method, where you pay off the highest interest debt first while making minimum payments on others, can save you significant money over time. Even small extra payments can make a big difference when interest rates are high.

- Identify: List all your debts with their respective interest rates.

- Target: Focus extra payments on the debt with the highest annual percentage rate (APR).

- Automate: Set up automatic payments to ensure consistency.

2. Consider Refinancing Select Loans

Refinancing involves taking out a new loan to pay off an existing one, ideally at a lower interest rate or with more favorable terms. While rising rates make refinancing less universally attractive, it can still be a powerful tool for specific situations, especially if your credit score has significantly improved or if you can move from a variable to a fixed rate at an opportune moment.

Mortgage Refinancing

If you have a variable-rate mortgage, or if your fixed-rate mortgage is coming up for renewal, exploring refinancing options is crucial. Even if rates are higher than historical lows, locking in a fixed rate now could protect you from future hikes. However, carefully weigh the closing costs against the potential savings. A ‘cash-out’ refinance, while tempting, adds to your principal and should be approached with extreme caution, especially in a high-rate environment.

Personal Loan Refinancing

If you have a variable-rate personal loan, or if your credit score has dramatically improved since you took out your current fixed-rate loan, refinancing could secure a lower rate. Shop around with various lenders to find the best terms.

Student Loan Refinancing

Private student loans with variable rates are prime candidates for refinancing, especially if you can secure a fixed rate. Federal student loans typically offer more protections and benefits, so refinancing them into a private loan should be considered very carefully, as you’d lose those federal benefits.

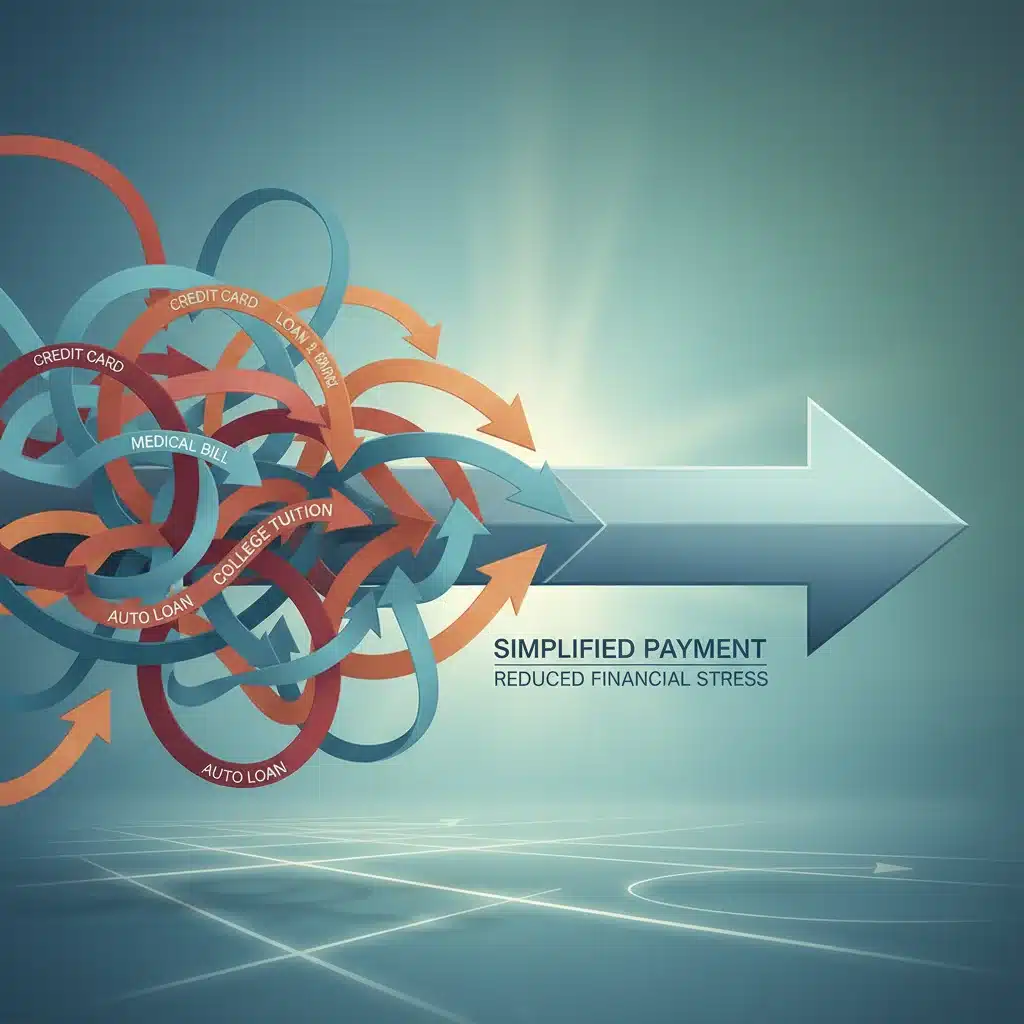

3. Debt Consolidation: Streamline and Save

Debt consolidation involves combining multiple debts into a single, new loan, often with a lower interest rate or a more manageable monthly payment. This can simplify your finances and reduce the overall interest paid, making it a key component of effective loan strategies.

Personal Consolidation Loans

These are unsecured loans that can be used to pay off high-interest credit card debt or other personal loans. If you have a good credit score, you might qualify for a rate significantly lower than your credit card APRs.

Balance Transfer Credit Cards

Some credit cards offer introductory 0% APR periods for balance transfers. This can be an excellent strategy to pay down high-interest debt without incurring additional interest for a set period. Be mindful of balance transfer fees and ensure you can pay off the transferred balance before the promotional period ends.

Home Equity Loans/Lines of Credit (HELOCs)

If you have substantial equity in your home, a home equity loan or HELOC can offer lower interest rates because they are secured by your home. However, this also means your home is collateral, and defaulting could lead to foreclosure. Use this option cautiously and only if you are confident in your repayment ability.

4. Make Extra Payments Whenever Possible

Even small, consistent extra payments can chip away at your principal faster, reducing the total interest paid over the life of the loan. This is especially effective for loans with daily interest accrual, like some mortgages. Consider directing bonuses, tax refunds, or unexpected windfalls towards your highest-interest debts.

5. Re-evaluate Your Budget and Spending Habits

In an environment of rising interest rates, every dollar counts. A thorough review of your budget can reveal areas where you can cut unnecessary expenses. The money saved can then be redirected towards accelerating debt repayment, thereby strengthening your loan strategies.

- Track Spending: Understand where your money is actually going.

- Identify Non-Essentials: Look for subscriptions, dining out, or entertainment costs that can be reduced.

- Create a Debt-Focused Budget: Allocate a larger portion of your income specifically to debt reduction.

6. Negotiate with Lenders

Don’t be afraid to contact your lenders, especially if you have a good payment history. They might be willing to offer a lower interest rate, waive fees, or adjust your payment schedule, particularly if you explain your commitment to paying off the debt and the challenges posed by rising rates. This is a often overlooked but effective part of loan strategies.

7. Understand the Terms of Your Loans

Many people sign loan agreements without fully understanding the fine print. Take the time to review your loan documents, paying close attention to:

- Interest Rate Type: Is it fixed or variable?

- Prepayment Penalties: Are there fees for paying off your loan early?

- Payment Schedule: How is interest calculated and applied?

- Fees: What are the late payment fees, annual fees, or other charges?

Knowing these details empowers you to make informed decisions and optimize your loan strategies.

8. Build an Emergency Fund

While not a direct loan strategy, a robust emergency fund provides a critical safety net. In times of economic uncertainty and rising costs, having 3-6 months of living expenses saved can prevent you from taking on new high-interest debt if unexpected expenses arise. This indirect strategy protects your financial progress and prevents setbacks.

9. Explore Income-Generating Opportunities

Increasing your income is another powerful way to combat rising interest rates. Consider a side hustle, negotiating a raise, or investing in skills that lead to higher-paying jobs. The additional income can be directly applied to your debts, accelerating your repayment and saving you interest.

Long-Term Planning: Beyond 2026

Effective loan strategies aren’t just about immediate adjustments; they’re about building resilience for the future. As you implement the strategies above, also think about your long-term financial goals.

Diversify Your Investments

If you have investments, consider reviewing your portfolio with a financial advisor. While rising rates can sometimes negatively impact certain asset classes, they can also present opportunities in others, such as higher yields on savings accounts and bonds.

Regular Financial Reviews

Make it a habit to review your financial situation at least annually. This includes checking your credit score, reviewing your budget, and assessing your debt repayment progress. This proactive approach ensures your loan strategies remain aligned with your financial goals and the prevailing economic conditions.

Educate Yourself Continuously

The financial world is constantly evolving. Stay informed about economic news, central bank policies, and new financial products. The more you know, the better equipped you’ll be to adapt your loan strategies and make sound financial decisions.

Common Misconceptions About Interest Rate Hikes

It’s easy to fall prey to misinformation or panic during periods of economic change. Let’s address some common misconceptions surrounding interest rate hikes and how they relate to your loan strategies.

Misconception 1: All Loans Are Equally Affected

As discussed, variable-rate loans are immediately impacted, while fixed-rate loans are not until renewal or if new borrowing occurs. Understanding this distinction is vital for targeted loan strategies. A fixed-rate mortgage holder might feel little immediate pain, while someone with significant credit card debt will see their costs soar.

Misconception 2: Refinancing is Always a Good Idea in a Rising Rate Environment

Not necessarily. If your current fixed rate is significantly lower than prevailing market rates, refinancing might mean taking on a higher interest rate. Refinancing is most beneficial when you can secure a lower rate, move from variable to fixed, or significantly improve loan terms. Always calculate potential savings versus costs.

Misconception 3: You Should Avoid All Debt During Rate Hikes

While minimizing unnecessary debt is always wise, some debt, like a mortgage for a primary residence, can be a necessary part of life and wealth building. The key is to manage debt responsibly and ensure it fits within your budget, even with higher interest costs. Strategic debt can still be beneficial; reckless debt is always problematic.

Misconception 4: The Economy Will Collapse Due to High Rates

Central banks raise rates to control inflation and prevent overheating, not to crash the economy. While there can be economic slowdowns, these measures are intended to create stability in the long run. Focusing on personal financial resilience through smart loan strategies is more productive than fearing widespread collapse.

Misconception 5: There’s Nothing You Can Do to Mitigate the Impact

This article is a testament to the opposite! There are numerous proactive steps you can take. From refinancing and consolidation to budgeting and extra payments, effective loan strategies can significantly reduce the financial burden of rising interest rates and lead to substantial annual savings.

Case Studies: Real-World Savings from Smart Loan Strategies

To illustrate the power of these loan strategies, let’s look at hypothetical scenarios:

Case Study 1: The Mortgage Holder

Sarah has a variable-rate mortgage of $300,000 at 5.5%. With anticipated rate hikes pushing it to 7.0% by 2026, her monthly payment would increase by approximately $270. By proactively refinancing into a fixed-rate mortgage at 6.5% (assuming she qualified for a slightly better rate due to improved credit), she saves $180 per month compared to the projected variable rate, totaling over $2,100 annually, and gains payment stability.

Case Study 2: The Credit Card Debt Conqueror

David carries $10,000 in credit card debt with an average APR of 22%. With rates rising, this could easily climb to 24-25%. He transfers his balance to a 0% APR balance transfer card for 18 months, with a 3% fee. By committing to paying $550 a month, he pays off the entire balance within the promotional period, avoiding thousands in interest payments he would have incurred at 22-25% APR, saving him approximately $2,000-$2,500 in interest alone over 18 months.

Case Study 3: The Consolidated Borrower

Maria has a mix of debts: a $5,000 personal loan at 12%, a $3,000 student loan at 8%, and a $4,000 car loan at 7%. Her combined monthly payments are high, and she’s struggling. She qualifies for an $12,000 debt consolidation loan at 9% for a 5-year term. While her car loan rate is slightly higher, the overall reduction in interest and the simplification of one monthly payment make it manageable. Over the 5 years, she saves about $800 in interest compared to her previous mix and significantly reduces stress.

Conclusion: Empowering Your Financial Future in 2026 and Beyond

The prospect of continued interest rate hikes in 2026 doesn’t have to be a source of dread. By adopting a proactive and informed approach to your loan strategies, you can not only mitigate the negative impacts but also seize opportunities to optimize your financial situation. Prioritizing high-interest debt, strategically refinancing, consolidating where beneficial, and meticulously managing your budget are all powerful tools at your disposal.

Remember, financial health is an ongoing journey. Regularly review your loans, assess the economic climate, and be prepared to adapt your loan strategies as needed. By taking these steps, you can confidently navigate the evolving financial landscape, protect your assets, and potentially save thousands of dollars annually, putting you on a stronger path to financial security.

Don’t wait for rates to hit their peak; start implementing these loan strategies today to secure your financial well-being for 2026 and the years to come.