Social Security Changes 2026: Your Guide to Upcoming Policy Shifts

Urgent Alert: Major Social Security Policy Changes Effective January 1, 2026 – What You Need to Know Now.

The landscape of retirement planning in the United States is constantly evolving, and a significant shift is on the horizon. As of January 1, 2026, a series of pivotal Social Security policy changes are slated to take effect, promising to reshape how millions of Americans approach their golden years. These aren’t minor adjustments; they represent fundamental alterations that could impact everything from your eligibility for benefits to the amount you receive and the strategies you employ for a secure retirement. Understanding these Social Security Changes 2026 is not just recommended, it’s absolutely crucial for anyone currently receiving benefits, nearing retirement, or even those just starting their careers.

This comprehensive guide aims to demystify the upcoming changes, providing you with a detailed breakdown of what to expect, how these modifications might affect your personal financial situation, and what proactive steps you can take today to navigate the new environment. We’ll delve into the specifics of the policy updates, explore their potential ramifications, and offer expert insights to help you prepare. Don’t wait until it’s too late; the time to understand and adapt to the Social Security Changes 2026 is now.

The Impetus Behind the Social Security Changes 2026

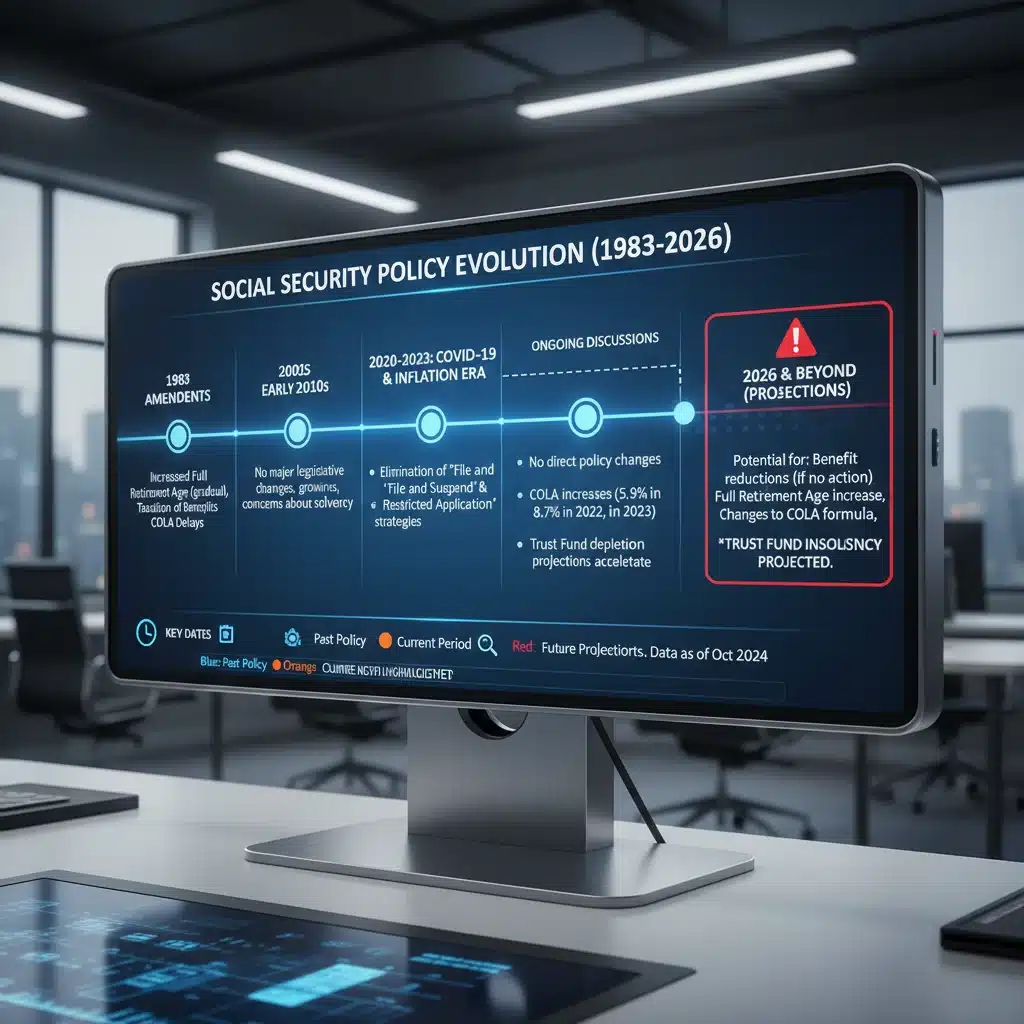

To truly grasp the significance of the Social Security Changes 2026, it’s essential to understand the forces driving them. Social Security, established in 1935, has served as a cornerstone of American retirement security for generations. However, demographic shifts, including increased life expectancy and declining birth rates, have placed considerable strain on the system’s long-term solvency. The ratio of workers contributing to the system compared to beneficiaries drawing from it has steadily decreased, leading to concerns about the program’s ability to meet its obligations in the decades to come.

For years, policymakers have debated various solutions to shore up the system. The upcoming Social Security Changes 2026 are the culmination of these discussions, representing a concerted effort to ensure the program’s sustainability for future generations. While the specifics are still being finalized in some areas, the overarching goal is to balance the needs of current and future beneficiaries with the economic realities of a changing workforce and population. These changes are not arbitrary; they are a direct response to actuarial projections and the need to maintain the integrity of a vital social safety net.

Understanding this context is vital because it highlights the necessity of these adjustments. While some changes may initially seem unfavorable, they are often designed to prevent more drastic measures down the line. By proactively addressing these challenges, the aim is to secure Social Security’s future, albeit with some modifications to the current framework. This forward-looking approach underscores the importance of staying informed and planning accordingly for the Social Security Changes 2026.

Key Policy Alterations: What’s Changing in 2026?

The core of the Social Security Changes 2026 lies in several key policy alterations. While the exact legislative language can be complex, we can identify several main areas that are likely to see significant modifications. These include, but may not be limited to, adjustments to the Full Retirement Age (FRA), changes in the calculation of benefits, modifications to the Cost-of-Living Adjustments (COLAs), and potential alterations to the earnings test for those working while receiving benefits.

Full Retirement Age (FRA) Adjustments

One of the most impactful Social Security Changes 2026 could be a further adjustment to the Full Retirement Age (FRA). Currently, the FRA varies depending on your birth year, gradually increasing from 65 to 67. There’s a strong possibility that the FRA could be pushed back even further for younger generations, potentially reaching 68 or even 69. This means that individuals born after a certain year would have to wait longer to receive their full benefits, or accept reduced benefits if they choose to claim earlier.

The rationale behind increasing the FRA is directly linked to increased life expectancy. As people live longer, they receive benefits for a longer period, placing a greater financial burden on the system. By raising the FRA, the government aims to reduce the total payout period for each beneficiary, thereby improving the system’s solvency. For you, this means re-evaluating your retirement timeline and potentially adjusting your savings strategy to account for a later start to full benefits.

Benefit Calculation Methodologies

Another area ripe for Social Security Changes 2026 is the methodology used to calculate your primary insurance amount (PIA), which determines your monthly benefit. While the fundamental calculation historically considers your highest 35 years of earnings, there could be modifications to how these earnings are indexed for inflation or how the bend points in the formula are applied. Even subtle changes in these calculations can have a substantial impact on the final benefit amount you receive.

For instance, policymakers might consider using a different inflation index, or altering the weighting of earlier earnings. These technical adjustments, though seemingly minor, can lead to a noticeable difference in your monthly Social Security check. Staying informed about these potential changes is crucial for accurately projecting your future retirement income and ensuring your financial plans remain robust.

Cost-of-Living Adjustments (COLAs)

Cost-of-Living Adjustments (COLAs) are designed to ensure that Social Security benefits retain their purchasing power over time, typically increasing annually to keep pace with inflation. However, the method for calculating COLAs could be subject to Social Security Changes 2026. There has been ongoing debate about whether the current Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) adequately reflects the spending patterns of seniors. Some proposals suggest shifting to a different index, such as the Consumer Price Index for the Elderly (CPI-E), which tends to show higher inflation for goods and services consumed by older Americans, particularly healthcare costs.

A change in the COLA calculation could significantly affect the long-term value of your benefits. A less generous COLA, for example, would mean your benefits increase at a slower rate, potentially eroding your purchasing power over time. Conversely, a more accurate or generous COLA could provide greater financial stability. Monitoring these discussions and understanding the potential impact on your annual benefit adjustments is a key aspect of preparing for the Social Security Changes 2026.

Earnings Test Modifications

For individuals who choose to work while receiving Social Security benefits before reaching their Full Retirement Age, the earnings test currently imposes limits on how much they can earn before their benefits are temporarily reduced. There’s a possibility that the thresholds for this earnings test, or even the reduction rates, could be altered as part of the Social Security Changes 2026. Such modifications could impact how many hours you choose to work in retirement or whether you decide to delay claiming benefits altogether.

A higher earnings limit would allow beneficiaries to earn more without penalty, providing greater flexibility in retirement. Conversely, a lower limit or a more aggressive reduction rate could incentivize earlier retirement or a greater reliance on other income sources. Understanding any changes to the earnings test is vital for those planning a phased retirement or who anticipate working part-time in their early retirement years.

Who Will Be Most Affected by the Social Security Changes 2026?

The impact of the Social Security Changes 2026 will not be uniform across the population. While everyone who relies on or contributes to Social Security will feel some effect, certain demographics and individuals at specific stages of their lives will experience more pronounced ramifications.

Near-Retirees (Ages 55-65)

Individuals who are within a decade of retirement are likely to be among the most immediately affected. For this group, changes to the Full Retirement Age could mean a sudden shift in their carefully laid plans. They might find themselves needing to work an extra year or two to receive their full benefits, or they may have to adjust their expectations regarding their monthly income if they choose to claim earlier. Changes in benefit calculation methodologies or COLAs could also directly impact the income they were anticipating for their initial retirement years.

For near-retirees, the urgency of understanding the Social Security Changes 2026 cannot be overstated. It’s a critical time to review existing retirement plans, consult with financial advisors, and make any necessary adjustments to savings, investments, or projected retirement dates.

Younger Generations (Under 40)

While the immediate impact on younger generations might seem less direct, they stand to be significantly affected in the long run. Any increases to the Full Retirement Age are primarily aimed at those currently further from retirement. Moreover, the long-term sustainability of the system, which these changes aim to address, is paramount for younger workers who will rely on Social Security decades from now. They might face a system with a higher FRA, potentially different benefit formulas, and possibly altered COLA mechanisms throughout their entire retirement.

For younger individuals, the Social Security Changes 2026 serve as a powerful reminder of the need for robust personal savings and diversified retirement planning. Relying solely on Social Security for future retirement income may become increasingly challenging, emphasizing the importance of 401(k)s, IRAs, and other investment vehicles.

Individuals with Lower Lifetime Earnings

Social Security has progressive benefit formulas, meaning it replaces a higher percentage of pre-retirement earnings for those with lower lifetime incomes. Therefore, any changes to benefit calculation methodologies or COLAs could disproportionately affect individuals who rely more heavily on Social Security as their primary source of retirement income. Even small reductions in projected benefits or slower growth due to COLA adjustments could have a more significant impact on their financial well-being.

This group may need to be particularly vigilant in understanding how the Social Security Changes 2026 might affect their safety net and explore all available resources for financial planning and support.

Proactive Steps to Take Now for Social Security Changes 2026

Given the impending Social Security Changes 2026, procrastination is not an option. Taking proactive steps now can significantly mitigate any potential negative impacts and ensure you are well-prepared for your financial future. Here are several key actions you should consider immediately:

1. Review Your Social Security Statement Annually

Your Social Security statement is a crucial document that provides an estimate of your future benefits based on your earnings record. It’s essential to review this statement annually for accuracy. Any errors in your earnings history could negatively impact your future benefits. With the Social Security Changes 2026 on the horizon, understanding your current estimated benefits provides a baseline against which to measure future adjustments.

You can access your statement online by creating an account at ssa.gov/myaccount. Regularly checking this will help you stay informed about your current standing and potential future changes.

2. Re-evaluate Your Retirement Timeline and Savings Goals

If the Full Retirement Age is adjusted or if benefit calculations change, your original retirement timeline or savings goals might need revision. Consider the possibility of working longer, increasing your contributions to retirement accounts, or exploring alternative income streams. The Social Security Changes 2026 underscore the importance of flexibility in retirement planning.

Use online retirement calculators and financial planning tools to model different scenarios. See how an extra year of work or an increase in savings could offset potential reductions in Social Security benefits.

3. Consult with a Financial Advisor

Navigating the complexities of Social Security policy and its interaction with your personal finances can be challenging. A qualified financial advisor specializing in retirement planning can provide invaluable guidance. They can help you understand the specific implications of the Social Security Changes 2026 for your situation, develop a tailored strategy, and integrate Social Security into your broader financial plan.

Look for advisors who are fiduciaries, meaning they are legally obligated to act in your best interest. They can help you explore options like delayed claiming strategies, investment adjustments, and other ways to optimize your retirement income.

4. Diversify Your Retirement Income Sources

Relying solely on Social Security for retirement income has always carried risks, and the Social Security Changes 2026 further highlight the importance of diversification. Maximize contributions to your 401(k), 403(b), IRA, or other employer-sponsored retirement plans. Explore other investment vehicles such as stocks, bonds, mutual funds, or real estate to build a robust and diversified retirement portfolio.

The more diverse your income streams, the less vulnerable you will be to any single policy change or economic downturn. This strategy provides a stronger foundation for financial security in retirement.

5. Stay Informed and Engaged

Policy discussions surrounding Social Security are ongoing. While the Social Security Changes 2026 are planned, further refinements or additional proposals could emerge. Stay informed by following reputable news sources, subscribing to updates from the Social Security Administration, and engaging with organizations focused on retirement security.

Understanding the evolving legislative landscape will allow you to anticipate future changes and adjust your plans accordingly. Knowledge is power, especially when it comes to securing your financial future.

6. Understand Spousal and Survivor Benefits

The Social Security Changes 2026 might also impact spousal and survivor benefits. If you are married or have dependents, it’s crucial to understand how these changes could affect your family’s overall financial security. For example, if the FRA increases, it could affect when a spouse can claim benefits based on your record, or the amount a surviving spouse might receive.

Review the rules for spousal and survivor benefits carefully. In some cases, strategic claiming decisions between spouses can significantly optimize total lifetime benefits. A financial advisor can help you navigate these complex rules in light of the upcoming changes.

Potential Long-Term Implications of the Social Security Changes 2026

Beyond the immediate adjustments, the Social Security Changes 2026 are likely to have profound long-term implications for American society and the economy. These shifts will influence retirement behaviors, personal savings rates, and the broader financial planning industry.

Shifting Retirement Expectations

With potential increases in the Full Retirement Age, the traditional notion of retiring in one’s mid-60s may become less common. More individuals might choose or need to work longer, leading to a gradual shift in retirement expectations and potentially a more experienced, older workforce. This could have both economic benefits, such as increased productivity, and social challenges, like competition for jobs between older and younger workers.

Increased Emphasis on Personal Savings

As Social Security benefits potentially undergo adjustments, the onus on individuals to save more for retirement will likely intensify. The Social Security Changes 2026 serve as a strong signal that personal savings, employer-sponsored plans, and other investments will play an even more critical role in ensuring a comfortable retirement. This could lead to higher savings rates across different age groups, particularly among younger generations who have more time to build their nest eggs.

Innovation in Retirement Products and Services

The financial services industry is likely to respond to the Social Security Changes 2026 by developing new products and services tailored to the evolving retirement landscape. This could include more flexible annuity options, specialized investment strategies for longer lifespans, and enhanced financial planning tools that account for later retirement ages and potentially modified Social Security benefits. Financial advisors will also need to adapt their expertise to guide clients through these new realities.

Impact on Social Equity

It’s also important to consider the social equity implications of the Social Security Changes 2026. While changes are necessary for solvency, some adjustments, such as increasing the FRA, can disproportionately affect individuals in physically demanding jobs or those with lower life expectancies. Policymakers will need to continuously evaluate the fairness and effectiveness of these changes and consider mechanisms to support vulnerable populations who may be more adversely impacted.

Conclusion: Preparing for Your Future with Social Security Changes 2026

The impending Social Security Changes 2026 are a critical development that demands your attention. While the specifics may continue to be refined, the underlying message is clear: the Social Security system is adapting to new demographic and economic realities, and so must your retirement planning strategy. By understanding the potential adjustments to the Full Retirement Age, benefit calculations, COLAs, and the earnings test, you can take proactive steps to safeguard your financial future.

Don’t be caught off guard. Take the time now to review your Social Security statement, re-evaluate your retirement goals, diversify your income streams, and consult with a trusted financial advisor. The path to a secure retirement in the face of these Social Security Changes 2026 lies in informed decision-making and proactive planning. Your future self will thank you for taking these vital steps today.